What Should You Do After Optimizing Your Credit Cards?

You found the right cards. You stopped overpaying annual fees. Maybe you switched a category or two and picked up an extra few hundred dollars a year in rewards. Good. That is real money, and capturing it is exactly what CardSavvy is for.

Now the harder question: what should those dollars actually do?

Summitward is our sister site, built by the same team. CardSavvy optimizes the payment layer. Summitward helps with the layer above it: net worth, financial independence, portfolio risk, taxes, and retirement. This post explains where one ends and the other begins, and why rewards are the smallest lever you have.

Where rewards rank against everything else

Here is the uncomfortable ranking. The things that decide your financial outcome, roughly in order of impact:

- Whether you carry credit card debt

- Your savings rate

- Your investment costs and taxes

- Your asset allocation and diversification

- Your own behavior under stress

- Your credit card rewards

Rewards come last. They are worth optimizing once everything above them is handled, and close to pointless before that.

The clearest case is debt. The average U.S. credit card rate on balances assessed interest is about 22% (Federal Reserve G.19). A great rewards setup might earn you 2% to 3% back. So a dollar of revolving balance costs you roughly seven to ten times what a dollar of optimized spending earns. If you carry a balance, paying it off beats any card strategy.

This is not a niche problem. The Federal Reserve found that 81% of adults had a credit card in 2024, and 46% of cardholders carried a balance at least once in the prior year (Economic Well-Being of U.S. Households). Revolving credit outstanding sits near $1.35 trillion. For a lot of people, the most valuable "rewards" move is to stop paying interest.

If you are still deciding whether you are ready to optimize at all, start with our readiness framework.

Where CardSavvy ends and Summitward begins

The two sites answer different questions at different scales.

| Dimension | CardSavvy | Summitward |

|---|---|---|

| Core question | Which card should I use, keep, cancel, or add? | Am I on track, and how should I manage investing, taxes, and retirement? |

| Decision level | Per purchase to annual | Multi-year to lifetime |

| Main user | Rewards optimizer, cardholder | DIY investor, FIRE-minded household |

| Main outputs | Best card by category, rewards value, fee and credit math | Net worth, FI projections, Monte Carlo, portfolio and factor analysis, Roth and tax planning |

| Risk it helps avoid | Wrong card, overpaid fees, overvalued credits | Bad assumptions, high fees, poor diversification, tax and sequence-of-returns mistakes |

CardSavvy works at the level of individual purchases. Summitward works at the level of your whole balance sheet. The bridge between them is a single question: once you know your rewards are worth $300 or $800 or $1,500 a year, does that change anything about your plan, and where should the money go?

What the research says

There is good evidence for spending your attention up the stack.

Fees compound quietly. The SEC's own illustration: a $100,000 portfolio over 20 years at a 4% return ends near $208,000 with a 0.25% annual fee, but only about $179,000 with a 1.00% fee. That $29,000 gap comes purely from fees (Investor.gov). One fee decision can dwarf a decade of careful rewards earning.

Active picking rarely wins. Over a 15-year horizon, roughly 9 in 10 actively managed U.S. large-cap funds underperformed the S&P 500, according to S&P's SPIVA scorecard. Low-cost, diversified, systematic investing is hard to beat, and most attempts to beat it cost money.

Behavior matters as much as product choice. Barber and Odean's research on household trading found that the most active traders underperformed the market by a wide margin. Frequent tinkering is expensive. A plan helps by making your assumptions explicit and catching mistakes before they compound.

Rewards themselves are an uneven transfer. Federal Reserve research on the credit card market found that rewards programs tend to benefit financially sophisticated users while leaving less sophisticated users worse off through higher borrowing. That makes rewards genuinely valuable for people who pay in full, and costly for people who do not. We have written before about who actually pays for rewards.

Education alone changes little; decision tools at the moment of choice do more. Meta-analyses of financial education find small average effects on behavior. What moves the needle is concrete, decision-specific tooling when a person is actually making the call. That is the whole design philosophy behind both of our sites, and behind our math-first promise.

Who Summitward is for

Summitward makes sense if you:

- Pay your card balances in full and treat rewards as optimization, not borrowing

- Already save and invest something, and want a clearer view of financial independence or portfolio risk

- Prefer DIY tools over paying an advisor 1% of assets for basic analytics

- Want to reason about taxes, Roth conversions, factor exposure, and long-term projections

Who should skip it for now

It is the wrong next step if you:

- Carry high-interest credit card debt (pay that off first, full stop)

- Overspend because of rewards or points chasing

- Want a simple transaction-budgeting app

- Need personalized legal, tax, or investment advice, or would be better served by a fiduciary planner for behavioral support or genuine complexity

We would rather say that plainly. A tool that tells you when to skip it is easier to trust.

What are your rewards actually worth?

The calculator below puts your rewards gain next to the two things that usually overshadow it: interest, if you carry a balance, and compounding, if you invest the difference. Enter your numbers and it will tell you the next best action.

The pattern is almost always the same. Say you improve your rewards by $500 a year. If you carry a $3,000 balance at 22%, that balance costs you $660 a year in interest and wipes out the entire reward, with money to spare. But if you pay in full and invest that $500 every year, at a 7% return over 30 years it grows to roughly $47,000. Same $500. Wildly different outcomes, decided entirely by the levers above rewards.

The bottom line

Use CardSavvy to capture the reward dollars you are already entitled to. Then use Summitward to decide whether those dollars, and the rest of your financial life, are actually moving you toward independence and long-term wealth.

Optimizing your wallet is worth doing. Deciding what to do with the money it frees up is the bigger question, and the one Summitward is built for.

Frequently Asked Questions

Are credit card rewards worth it? Yes, if you pay in full every month. If you carry a balance, interest near 22% usually erases the benefit, so paying off debt comes first.

What matters more than rewards? Avoiding interest, keeping investment fees low, allocation, taxes, your savings rate, and your behavior. Rewards sit on top of a sound plan; they do not replace one.

How much do investment fees cost? On a $100,000 portfolio over 20 years at a 4% return, the SEC's example shows about $179,000 at a 1.00% fee versus $208,000 at 0.25%, a $29,000 difference from fees alone.

Is Summitward free, and is it affiliated with CardSavvy? Summitward is our sister site, built by the same team, for DIY investors. There is no affiliate relationship between the two sites. We link to it because it answers the question CardSavvy cannot.

Who should not use a planning tool yet? Anyone carrying high-interest debt, overspending, or needing personalized advice. Pay down debt first; planning tools help most once the basics are handled.

Related on Learn

Hand-picked based on topic and reader interest

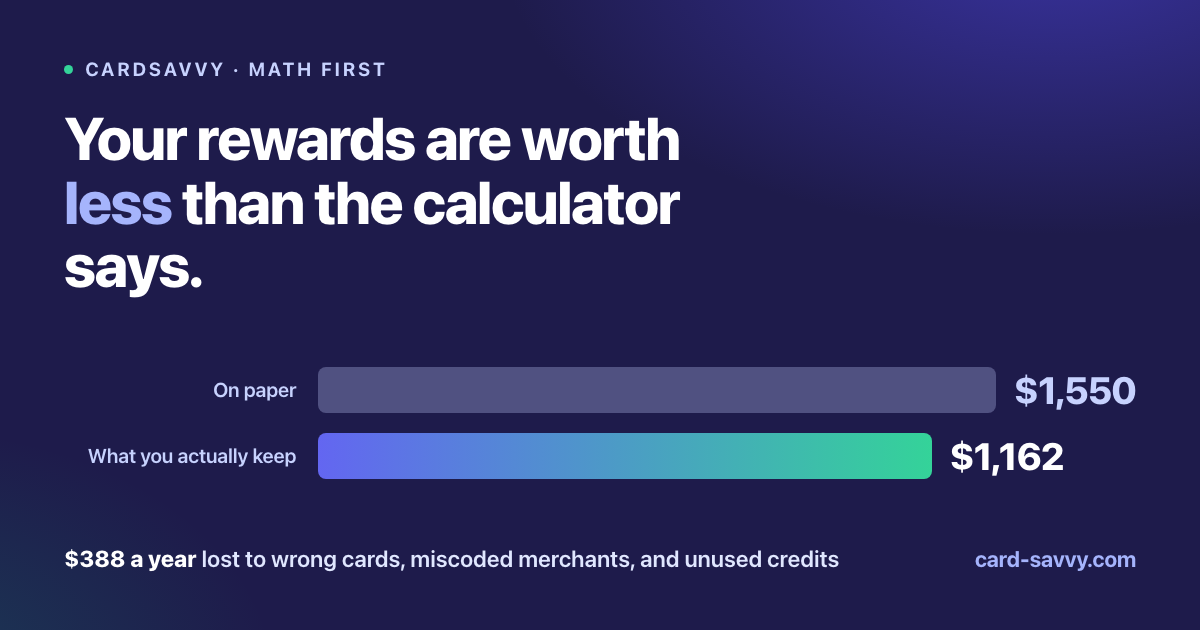

Why Your Credit Card Rewards Are Worth Less Than the Calculator Says

The optimization math is solved. Getting the money is not. Seven measurable gaps between the rewards a calculator promises and the value you actually keep, with the number attached to each.

The Summer Vacation Credit Card Audit: Rewards, Fees, Credits, and Interest

A repeatable summer travel credit card audit: check whether your card beat a 2% card after fees, the credits you used, interest, and foreign fees, plus the travel protections and refund rights most guides skip.

The 4th of July Credit Card Hangover: A 15-Minute Summer Rewards Audit

You already spent the money on July 4 travel, gas, and dining. Here's a 15-minute audit to check whether your cards earned what they should have, avoid interest, and set up the rest of summer.

The 2-Card Wallet That Beats 90% of Trifectas

Stop juggling 5 cards. We break down three 2-card setups that mathematically outperform most complex trifectas—with half the mental overhead.

Get smarter with your cards

Math-first card strategy posts, sent when we publish — not on a schedule. No spam. Unsubscribe anytime.

We respect your inbox.

Ready to optimize your wallet?

Get personalized card recommendations and spending strategies in under 2 minutes.

Free to use. No signup required.

Get My Strategy →Just need an answer for one purchase? Best Card →